One of the easiest ways to save money on your mortgage is to pay it off faster.

Most Canadian mortgages include prepayment privileges that allow homeowners to put extra money toward their mortgage principal without paying a penalty. The more principal you pay off early, the less interest you’ll pay over the life of your mortgage.

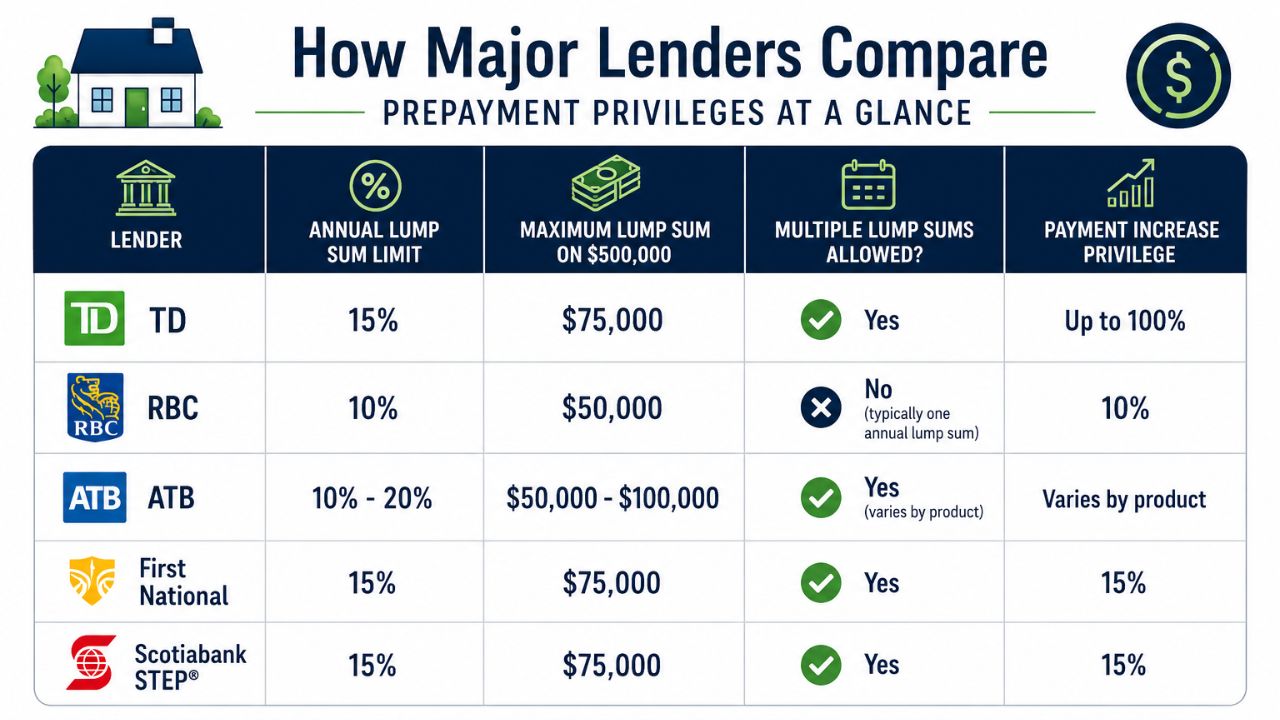

The challenge is that every lender has different rules regarding how much extra you can pay and how often you can make those payments.

Two Ways to Pay Down Your Mortgage Faster

Most lenders offer two main ways to accelerate your mortgage repayment:

1. Lump Sum Payments

A lump sum payment is a one-time payment applied directly to your mortgage principal.

Many homeowners use bonuses, commissions, tax refunds, inheritances, or investment proceeds to make lump sum payments. These can be as little as $100.

2. Payment Increases

Most lenders also allow borrowers to increase their regular mortgage payment by a certain percentage. This can be a simple way to pay down your mortgage faster because the extra amount is automatically applied with every payment. And if you ever need to bring that payment back down again, you can (to a minimum of the originally agreed amount.)

Importantly, payment increases and lump sum privileges are usually separate benefits. In most cases, increasing your monthly payment does not reduce the amount you’re allowed to contribute through lump sum payments.

How the Major Lenders Compare

Here’s a comparison of common prepayment privileges offered by several major lenders.

The Power of Increasing Payment Amounts

Lump sum payments tend to get most of the attention, but payment increases can be just as powerful.

Let’s say your mortgage payment is $2,500 per month. If your lender allows a 15% payment increase, you could raise your payment to $2,875 per month. That would direct an additional $4,500 toward your mortgage every year without having to plan a lump sum payment.

TD stands out in this category because it allows payment increases of up to 100% of the original payment amount on many mortgage products.

Which Strategy Is Better?

The answer depends on how you get paid. If you receive bonuses, commissions, or other irregular income, lump sum payments may make the most sense. If your income has increased permanently and you want a simple set-it-and-forget-it approach, increasing your regular mortgage payment may be the better option.

Many homeowners use both strategies together. For example, someone might increase their monthly payment after receiving a raise while also applying annual bonuses as lump sum payments.

What Homeowners Should Take Away From This

Most borrowers focus on interest rates when comparing mortgages. However, prepayment privileges can have a significant impact on how quickly you become mortgage-free.

Before signing a mortgage, take a few minutes to understand:

- How much you can contribute through lump sum payments

- Whether multiple lump sums are allowed

- How much you can increase your regular payment

- Whether those privileges are separate from one another

The answers vary by lender, and those differences can have a meaningful impact on your ability to pay down your mortgage faster. To get started on your mortgage journey, contact me.