When Marcus and Elena* first reached out, they weren’t asking about debt. They were asking about moving.

Like a lot of Calgary and Edmonton homeowners over the past couple of years, they’d watched the cost of nearly everything climb — groceries, vehicles, credit card interest — and their balances had crept up right along with it. Two vehicle loans, a few credit cards, a couple of lines of credit. On their own, each payment felt manageable. Added together, they came to more than $3,290 every single month on top of the mortgage.

Their plan was to sell the family home and “downsize” somewhere else in their North Calgary suburban community to free up some breathing room. It’s a completely understandable instinct — when the pressure builds, moving feels like the reset button. But when we actually ran the numbers, the plan started to fall apart.

The turning point: they didn’t know refinancing was an option

Here’s the part that surprised them most. Marcus and Elena genuinely believed the only way to pull equity out of their home to deal with the debt was to sell it. They didn’t know that a refinance — replacing their existing mortgage with a new, larger one and rolling the debt into it — was even on the table.

They love their home. They’d put a solid down payment on it a few years earlier, the property had gone up in value, and they’d chipped away at the mortgage the whole time. All of that had quietly built into real equity. The house wasn’t the problem — it was actually the solution.

“They had no reason to leave their home. They just needed a way to use it.”

What we actually did

Valued the home & equity

With the home worth about $600,000, there was plenty of room to refinance while staying well within lender limits.

Rolled the debt in

We consolidated $105,480 of credit cards, lines of credit and vehicle loans into one new mortgage of $406,000.

One simple payment

Six monthly payments became one. Their mortgage went up modestly — their total monthly outflow dropped dramatically.

| What it was | Balance | Monthly payment |

|---|---|---|

| Credit card | $8,694 | $260.82 |

| Line of credit | $17,578 | $425.00 |

| Credit card | $34,481 | $1,034.43 |

| Installment loan | $16,573 | $497.19 |

| Line of credit | $21,961 | $658.83 |

| Vehicle loan | $6,193 | $413.83 |

| Total rolled into the mortgage | $105,480 | $3,290.10 |

Six separate high-interest payments — consolidated into one mortgage payment at a far lower rate.

The before & after that made it a no-brainer

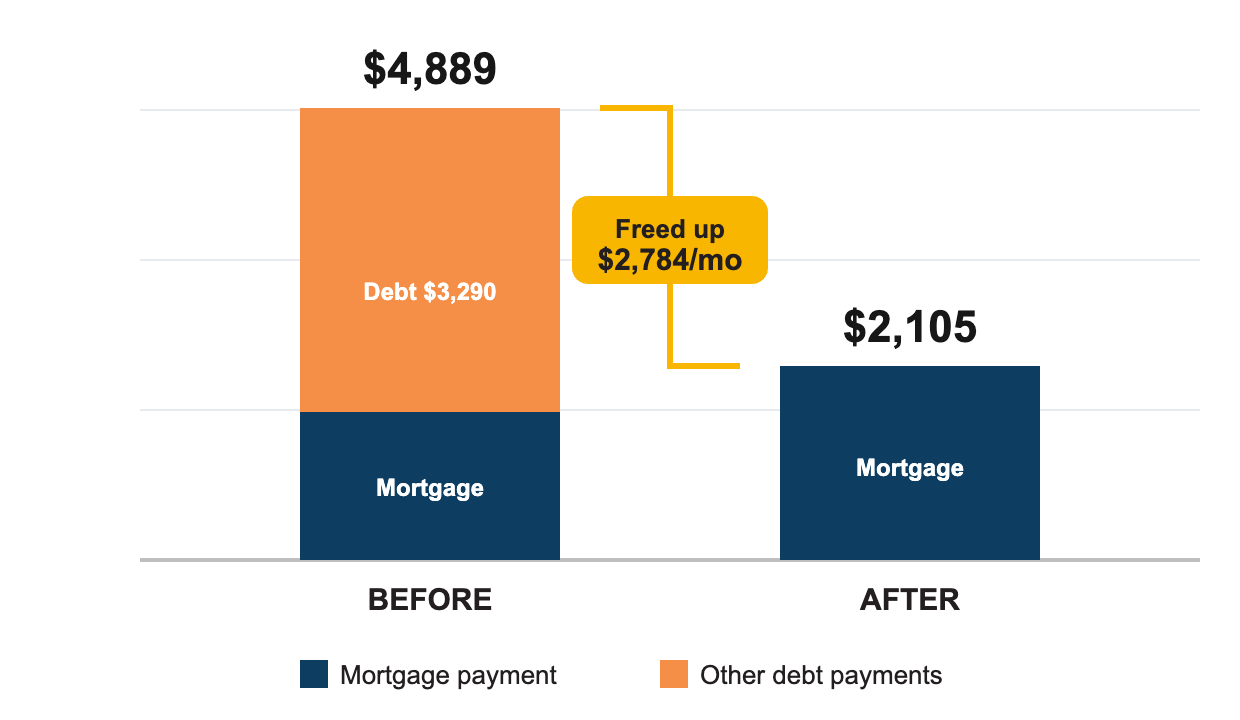

The key isn’t just that the debt disappeared — it’s what happened to the family’s monthly cash flow. Yes, the mortgage payment went up by about $506 a month. But it replaced more than $3,290 in other payments. Here’s the whole picture side by side:

| Monthly obligations | Before | After |

|---|---|---|

| Mortgage payment | $1,599 | $2,105 |

| Credit cards, loans & lines of credit | $3,290 | $0 |

| Total out the door each month | $4,889 | $2,105 |

A single mortgage payment of $2,105 replaced $4,889 in combined monthly payments.

That’s roughly $2,784 a month — about $33,400 a year — back in the family’s pocket. And the new mortgage of $406,000 on a $600,000 home left them at about a 68% loan-to-value, comfortably inside the 80% limit lenders allow on a refinance, with roughly $194,000 of equity still in the home.

The move would have cost them — for nothing

It’s worth spelling out what selling would have actually meant. On a $600,000 home, a realtor’s commission alone typically runs $20,000–$25,000. Add legal fees, moving costs, and the sheer stress of staging a house, living out of boxes, and uprooting the family — all to end up in a similar home in the same community, carrying the same debt.

Could this work for you?

This isn’t a rare, everything-lined-up-perfectly story. It’s one of the most common wins we see for Alberta homeowners right now. You may be a strong candidate for a debt-consolidation refinance if:

- You own a home in Calgary, Edmonton, or elsewhere in Alberta

- Your home has gone up in value and/or you’ve paid down your mortgage since you bought

- You’re carrying higher-interest debt — credit cards, lines of credit, vehicle or consumer loans

- Your monthly payments feel heavier than they used to, and cash flow is tight

- You’d rather stay in your home than sell to deal with debt

Every file is different — rates, penalties, equity and qualifying all vary from person to person. The only way to know what’s possible for your situation is to run your numbers. That part is free, and there’s no obligation.

See if a refinance could free up your cash flow

Find out how much high-interest debt you could consolidate — and how much you could put back in your pocket each month. It takes minutes to start, and we’ll do the math for you.

Apply for a Refinance → Serving Calgary, Edmonton & all of Alberta · Mortgages for Less with INDI MortgageRefinancing to consolidate debt: common questions

What is a debt-consolidation refinance?

How much equity do I need to refinance in Alberta?

Will my monthly payments really go down?

Does rolling debt into my mortgage mean I pay more interest overall?

What does it cost to refinance?

Do I have to sell my home to access my equity?

I’m in Edmonton or a smaller Alberta town — can you still help?

How do I find out if this could work for me?

*Names and identifying details have been changed to protect client privacy. This case study is based on a real client file; the dollar figures shown reflect that file and are provided for illustration only. Every mortgage situation is different — rates, penalties, equity, qualification and results vary by individual and by lender, and are subject to change and to lender approval. Maximum refinance amounts in Canada are generally limited to 80% of a home’s appraised value. This article is general information, not financial, mortgage or legal advice. Please speak with a licensed mortgage professional about your specific circumstances. Mortgages for Less with INDI Mortgage.