Most people assume private lending is only for borrowers in serious trouble. As a mortgage broker in Alberta, I can tell you that in reality, some of my most financially responsible clients use private mortgages on purpose.

Banks are designed for predictable situations. If your income, timeline, or property fits a standard checklist, they work well. But real life doesn’t always follow a checklist. When timing, paperwork, or property details fall outside the box, a private mortgage can become a practical tool — not a last resort.

Below are five situations where private lending can genuinely be the smarter option.

Avoiding a Large Mortgage Penalty

Breaking a mortgage early with a big bank can be expensive. I regularly see penalties in the tens of thousands of dollars.

Sometimes clients need access to equity now, but renewing or refinancing with their bank triggers that penalty. In the right situation, a short-term private second mortgage can provide the funds they need while waiting for the penalty window to pass.

Instead of paying a large fee to the bank, they use a temporary solution and save money overall. This is not about avoiding responsibility — it’s about timing the financing properly.

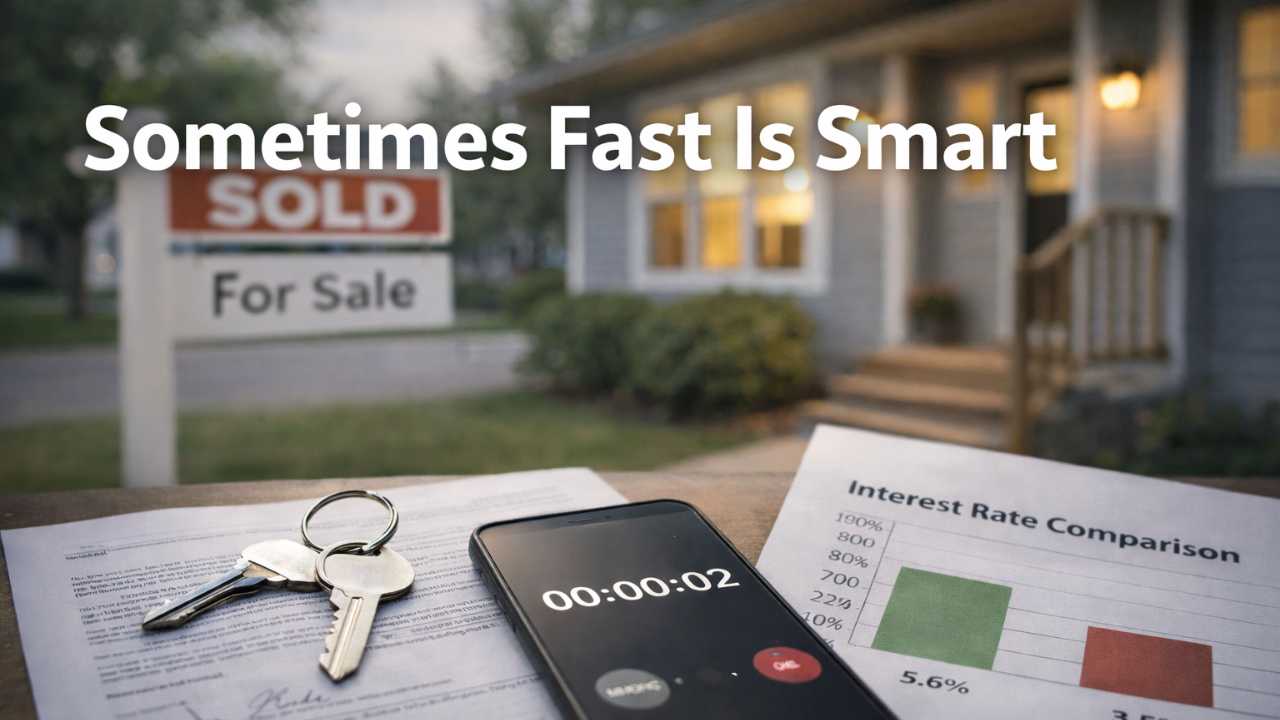

When Speed Matters More Than Rate

Banks move carefully. That’s good for risk control, but not helpful when a purchase closes in a few days.

In Alberta’s market, I occasionally see opportunities where a seller accepts an offer with a very fast possession date. Maybe it’s an estate sale, a relocation, or a distressed property. Waiting two to three weeks for a traditional approval means losing the home.

Private lending can fund in about 24 hours once approved. It costs more in interest, but sometimes the opportunity itself is worth far more than the short-term cost.

The cheapest mortgage is not always the best mortgage if you miss the property entirely.

Self-Employed or Complex Income

Self-employed borrowers often have strong businesses and solid assets but complicated income on paper. Tax planning reduces reported income, which helps with taxes but hurts traditional mortgage approval.

Banks lend based on documented income. Private lenders lend based on equity and overall strength.

A private mortgage can act as a bridge. We use it short-term while preparing cleaner financials, filing updated returns, or establishing a longer income history. Later, we move the client back into a conventional mortgage at a lower rate.

Unique or Rural Properties

Not every Alberta property fits a bank’s comfort zone. Examples include:

- rural homes with wells or septic systems

- mixed residential and commercial use

- acreages

- non-standard construction

- properties needing repairs

These homes can be perfectly livable and valuable, but banks see additional risk. A private lender evaluates the equity and marketability instead of rejecting the file automatically.

This often allows buyers to secure the property first, then refinance with a traditional lender once improvements or documentation are complete.

Rebuilding Credit After Financial Hardship

Bankruptcy, consumer proposals, and past credit problems don’t last forever, but they do temporarily limit mortgage options.

Many homeowners still have strong equity even though their credit is recovering. A private mortgage can provide time to rebuild credit history while keeping or accessing their home.

After 12 to 24 months of improved payment behaviour, we typically refinance into a standard mortgage at a much better rate. The private mortgage is the bridge, not the destination.

Private Lending Is a Strategy, Not a Failure

A private mortgage is a short-term financial tool. Smart borrowers use it to:

- avoid large penalties

- buy time for documentation

- secure a property quickly

- access equity

- transition back to traditional financing

The key is having a clear exit plan from day one. I never recommend private lending without knowing exactly how we will leave it. In the right situation, it can solve a problem that banks simply aren’t built to handle.

If your situation doesn’t fit neatly inside a bank application, that doesn’t mean homeownership or refinancing is impossible. It just means we need the right strategy first, and the best rate second. Reach out and we can build a plan suited to your specific needs.