If you’re buying your first home, it can feel like there are a hundred decisions to make all at once. One of which is:

Should I talk to a mortgage broker before I start house shopping, or after I find a home I like?

Both approaches happen all the time. But they can lead to very different experiences.

In this article, I’ll walk you through both options with the goal to help you understand which one fits your situation best so you can move forward with confidence.

Talking to a Mortgage Broker BEFORE House Shopping

This means you speak with a mortgage broker before you start going out and booking walk-throughs. In most cases, this involves getting a pre-approval.

Here’s how it works:

- You share your income, savings, and debts

- We review your credit and financial picture

- We estimate how much you can afford

- You get a price range and often a pre-approval letter

In this scenario, you know your budget upfront and understand your monthly payments early, allowing you can shop with confidence.

Many first-time buyers want clarity before they start. They don’t want to fall in love with a home they can’t afford. This approach helps avoid surprises.

Talking to a Mortgage Broker AFTER House Shopping

This is when you start looking at homes first, and only speak to a mortgage broker once you’re ready to make an offer—or after you already have.

Here’s how it works:

- You browse listings and attend showings

- You find a home you like

- Then you reach out to a broker to arrange financing

In this scenario, since you focus on the home first and financing comes later, timing can end up tighter. Some people want to “see what’s out there” before thinking about financing. Others assume the mortgage step is quick and can be handled later.

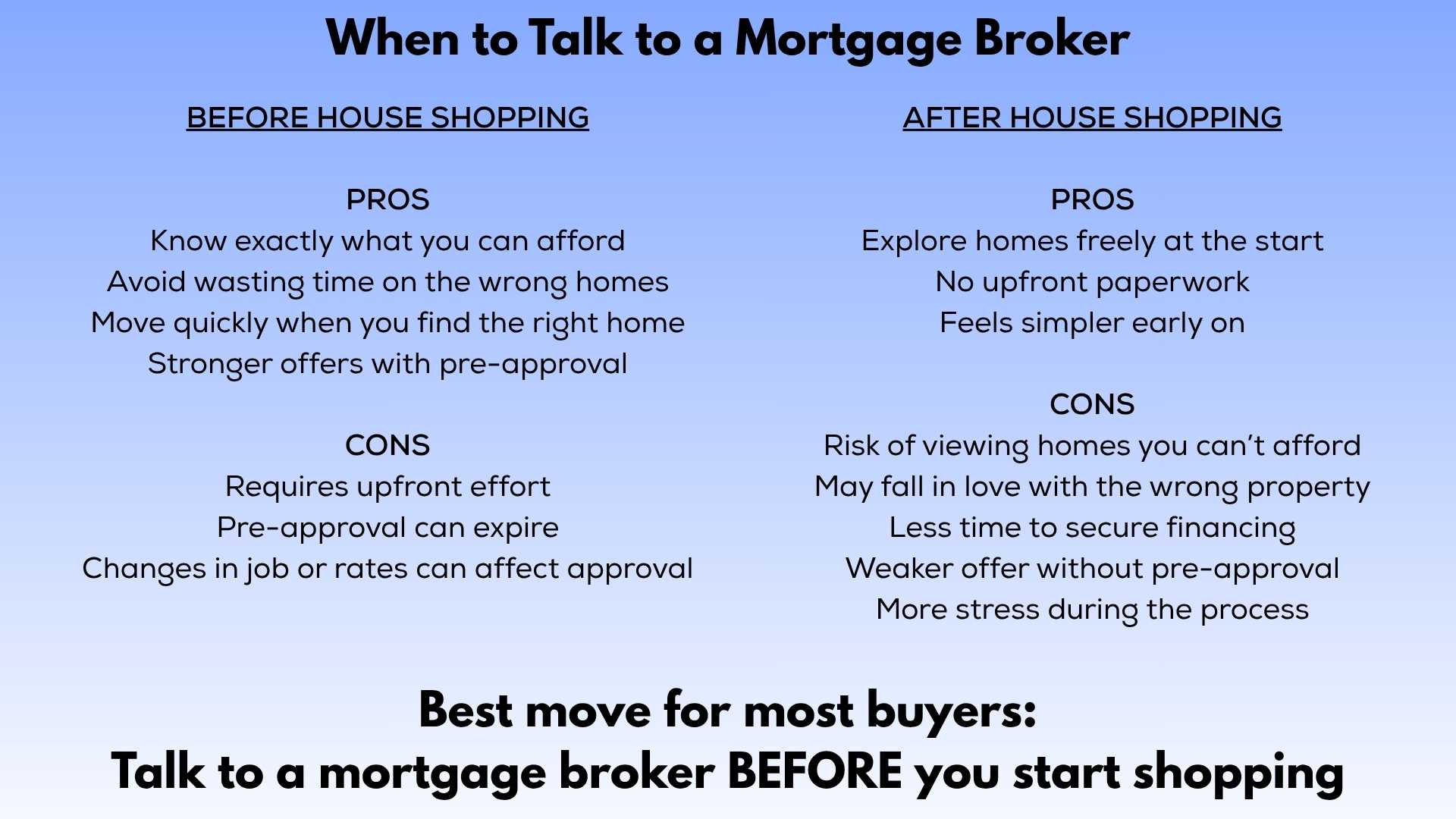

The Pros and Cons

Advice BEFORE shopping Pros

When you talk to a mortgage broker before house shopping, you know exactly what you can afford right from the start and avoid wasting time looking at homes that are outside your budget. You can act quickly when you find the right home because you’ll know what you qualify for and can afford, and sellers will take you more seriously.

Advice BEFORE shopping Cons

Talking with a mortgage broker first does require a bit of upfront effort. Additionally, your pre-approval may expire if you take too long to buy, or it may no longer qualify if you have employment changes or if rates change.

Advice AFTER shopping Pros

You can explore homes freely at the start, there’s no upfront paperwork, and it makes the earlier stages feel simpler.

Advice AFTER shopping Cons

Waiting to talk to a mortgage broker until after you’ve started house hunting may lead you to viewing homes you can’t actually afford so you risk falling in love with a property outside of your budget. Once you do set your heart on a property, you will have less time to secure financing after making an offer, which may be weaker without a pre-approval. All of this can cause higher stress during the purchase process.

Which Option Is Better for First-Time Buyers?

In most cases, talking to a mortgage broker before house shopping is the better choice. But let’s look at real situations.

When income stability is questionable

If your income varies (self-employed, commission, new to Canada), it’s especially important to talk to a broker early. We can confirm what lenders will actually accept.

When affordability is your main concern

If you’re trying to stay within a tight budget, knowing your numbers upfront is critical. It helps you avoid stretching too far.

When you want flexibility

If you’re just casually browsing and not ready to buy yet, it can be okay to look first. But I still recommend at least a quick conversation so you have a rough idea of your limits.

When the market is competitive

In fast-moving markets, pre-approval gives you a real advantage. You can move quickly and confidently when the right home comes up.

The Mistake Many First-Time Buyers Make

Buyers assume getting a mortgage is quick and easy, so they leave it until the last minute. That may be true from some, but in reality, financing can take time—especially if your situation is even slightly complex.

Things that take time include:

- Income verification

- Down payment sourcing

- Credit checks

- Lender requirements

These can all slow things down. I’ve seen buyers find the perfect home, only to run into stress (or even lose the deal) because they didn’t sort out financing early.

How a Mortgage Broker Helps You Decide

A big part of my job isn’t just finding you a rate. It’s helping you understand your options.

When we talk early, I can help you understand your true price range, estimate your monthly payments, and plan your down payment strategy. All of which allows us to avoid surprises.

If you come to me later in the process, I can still help—but we’re often working under tighter timelines. Either way, the goal is the same: to make sure your mortgage fits your situation, not just the property.

My Advice

In most cases, talking to a mortgage broker before house shopping makes the process smoother, less stressful, and more predictable. It helps you shop with confidence and avoid costly surprises. The best next step is understanding what your mortgage options actually look like. Contact me to find out.