If you’ve been shopping for a mortgage, you may have noticed that lenders often advertise one interest rate but offer another. You might see a bank showing a posted rate of 6.49%, but when you speak with someone, you’re told you may qualify for a much lower rate, such as 4.29%.

So which rate matters? The answer is both. The discounted rate usually affects your monthly payment, but the posted rate can still matter in other ways, especially if you break your mortgage before the end of the term.

What Is a Posted Rate?

A posted rate is the standard mortgage rate published by a lender. You can think of it as the lender’s sticker price. Banks and other lenders usually post rates for different mortgage terms, such as one-year, three-year, and five-year fixed mortgages.

In reality, very few qualified borrowers actually pay the posted rate. Most borrowers receive some type of discount from the lender. That discount is what brings the mortgage rate down to the rate the borrower actually receives.

For example, a lender may have a posted five-year fixed rate of 6.49%. If the lender offers you a 2.20% discount, your actual mortgage rate would be 4.29%. That 4.29% rate is the rate used to calculate your mortgage payment.

What Is a Discounted Rate?

A discounted rate is the actual mortgage rate being offered to you. This is the rate most borrowers focus on because it directly affects the payment, interest cost, and affordability of the mortgage.

When someone says they received a 4.29% mortgage rate, they are usually talking about the discounted rate, not the posted rate. This is the number that matters most for your monthly budget.

However, just because two lenders offer the same discounted rate does not mean the mortgages are the same. The fine print can be very different from one lender to another.

Why Do Lenders Have Posted Rates?

Many borrowers wonder why posted rates exist at all if most people don’t pay them. One reason is that posted rates give lenders a benchmark. A lender can publish a standard rate and then apply discounts based on the borrower, product, term, market conditions, or internal pricing.

Posted rates may also be used in some mortgage penalty calculations. This is where they can become very important. A borrower might not care much about the posted rate when they first get the mortgage, but they may care a lot if they need to sell, refinance, or switch lenders before the term is finished.

Posted Rates and Mortgage Penalties

If you break a fixed-rate mortgage early, your lender may charge a penalty. In many cases, the penalty is calculated using either three months’ interest or something called the Interest Rate Differential, often referred to as IRD.

The exact IRD formula varies by lender. Some lenders use posted rates in their calculation, while others use different methods. This is one of the reasons mortgage penalties can vary so much from one lender to another.

A borrower who received a large discount from a lender’s posted rate may be surprised by how that discount affects the penalty later. This does not mean a discounted rate is bad. It simply means the borrower should understand how the lender calculates penalties before signing.

Why the Lowest Rate Isn’t Always the Best Mortgage

Most people naturally want the lowest rate possible. That makes sense. A lower rate can reduce your payment and save interest. However, the lowest rate is not always the best mortgage.

A good mortgage should fit your life, not just your rate expectations. It is important to consider prepayment privileges, penalty calculations, portability, refinance options, payment increase privileges, and how flexible the lender is if your situation changes.

For example, if you plan to stay in your home for the full term, penalty flexibility may not seem important. But if there is a chance you could move, refinance, separate, upgrade, downsize, or need to access equity, the penalty calculation could matter a lot.

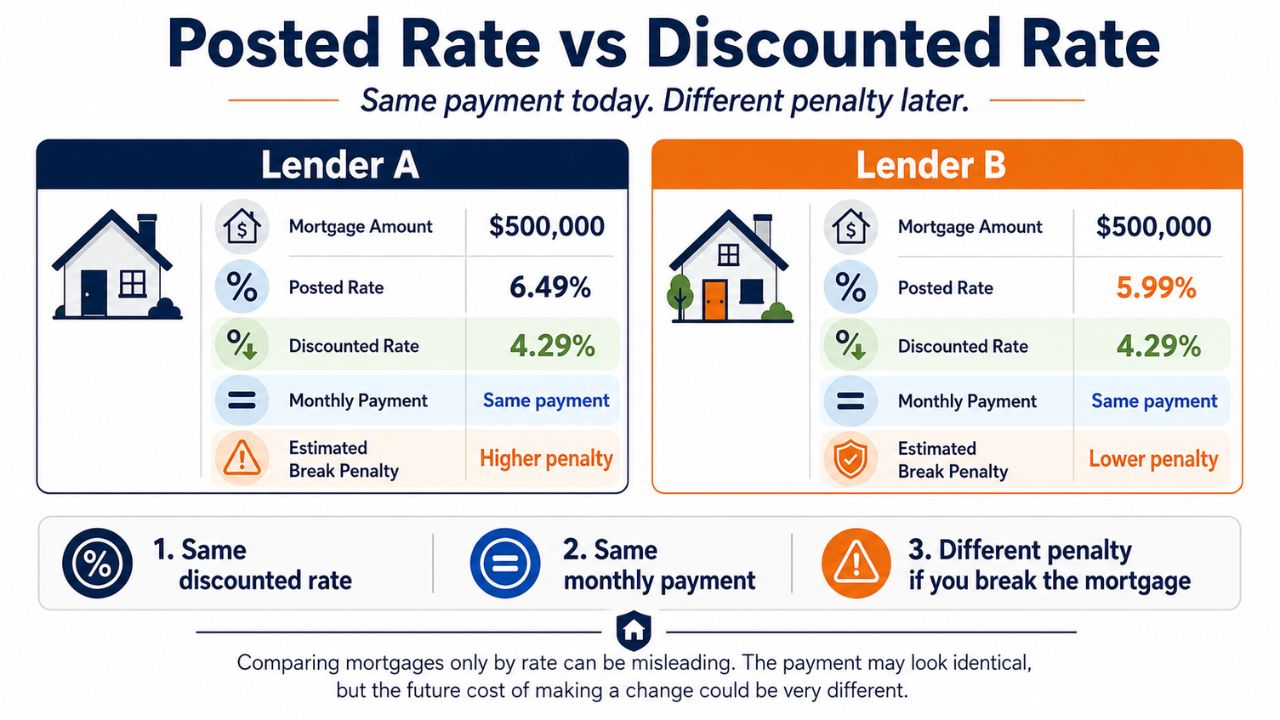

An Example

Let’s say two borrowers each have a $500,000 mortgage at an actual discounted rate of 4.29%. Their payments may be the same because the contract rate is the same.

However, one lender may have started with a posted rate of 6.49%, while another lender may have started with a posted rate of 5.99%. If both borrowers break their mortgages early, the penalties may not be the same because each lender may calculate the penalty differently.

This is why comparing mortgages only by rate can be misleading. The monthly payment may look identical, but the future cost of making a change could be very different.

In a Nutshell

The discounted rate is the rate that affects your mortgage payment today. The posted rate may affect your mortgage penalty later. That is why it is important to understand both. Before choosing a mortgage, make sure you know not only the rate being offered, but also how the lender handles penalties, prepayments, portability, and flexibility.

A mortgage broker like me can help you compare those details so you are not just choosing the lowest rate, but the mortgage that best fits your plans. Contact me for free personalized advice.