Many homebuyers assume that a variable-rate mortgage and an adjustable-rate mortgage are the same thing. They’re not. While both types of mortgages are tied to changes in a lender’s prime rate, they work differently when interest rates move. Understanding the difference can help you choose the mortgage that best fits your budget and comfort level.

What Is a Variable-Rate Mortgage?

With a traditional variable-rate mortgage, your interest rate changes whenever your lender changes its prime rate. However, your mortgage payment typically stays the same.

When rates fall, more of your payment goes toward paying down the mortgage principal and less goes toward interest. When rates rise, more of your payment goes toward interest and less goes toward principal. The amount you pay each month usually remains unchanged unless rates rise significantly.

Many borrowers appreciate the stability of knowing exactly what their payment will be each month, even though the balance between interest and principal changes over time.

What Is an Adjustable-Rate Mortgage?

An adjustable-rate mortgage also follows changes in prime rate, but the payment changes whenever rates change.

If rates increase, your payment increases. If rates decrease, your payment decreases. Because the payment adjusts immediately, your mortgage stays on its original amortization schedule.

Many lenders now offer adjustable-rate mortgages instead of traditional variable-rate mortgages. While the rates may appear similar, the payment experience can be very different.

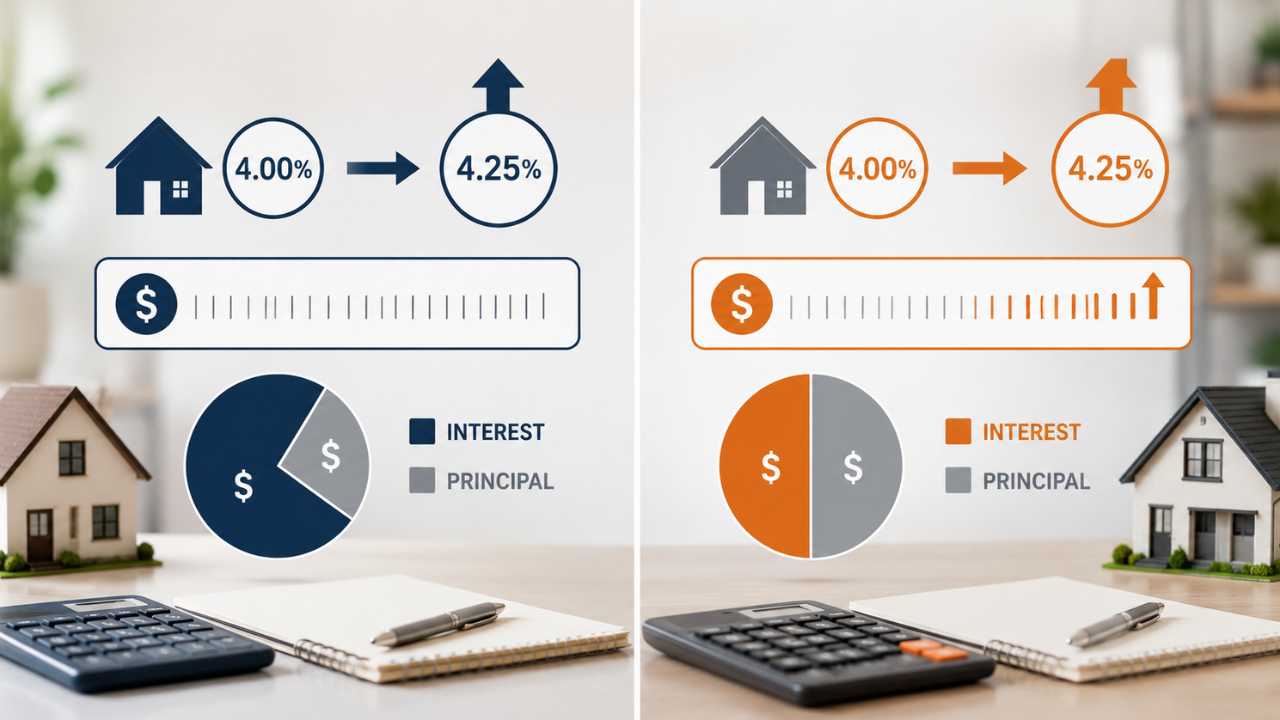

An Example

Let’s assume you have a $500,000 mortgage with an interest rate of 4.00%.

If rates increase by 0.25%, a traditional variable-rate mortgage would usually keep the payment the same. More of the payment would go toward interest and less toward principal, which could slow down how quickly the mortgage is paid off.

With an adjustable-rate mortgage, the payment would increase to keep the mortgage on schedule. The interest rate change is the same in both cases. The difference is how the lender handles the payment.

What Is a Trigger Rate?

Many Canadians became familiar with trigger rates during the rapid rate increases of 2022 and 2023.

A trigger rate occurs when so much of a variable mortgage payment is going toward interest that little or none is going toward principal. At that point, the lender may require a payment increase, a lump-sum payment, or other changes to bring the mortgage back on track.

This situation generally applies to traditional variable-rate mortgages with fixed payments. Adjustable-rate mortgages avoid this issue because the payment changes whenever rates move.

Which Option Is Better?

Neither option is automatically better. The right choice depends on your preferences and financial situation.

A traditional variable-rate mortgage may appeal to borrowers who prefer stable monthly payments. Even if rates change, your payment usually stays the same.

An adjustable-rate mortgage may appeal to borrowers who want their mortgage to remain on its original amortization schedule. The trade-off is that payments can rise or fall whenever interest rates change.

What Happens When Rates Fall?

When rates decrease, both mortgage types benefit.

With a variable-rate mortgage, the payment usually stays the same, but more of each payment goes toward principal. This can help you pay off your mortgage faster. With an adjustable-rate mortgage, the payment decreases, improving monthly cash flow while keeping the amortization unchanged.

Some borrowers prefer seeing a lower payment when rates fall, while others like knowing the savings are helping them become mortgage-free sooner.

What About Alberta Homeowners?

Many Alberta homeowners are currently deciding between fixed and variable rates as they approach renewal. If you’re considering a variable option, it’s important to understand whether the lender is offering a traditional variable-rate mortgage or an adjustable-rate mortgage.

Different lenders use different terminology, and many borrowers don’t realize there is a difference until rates begin moving. Before signing a mortgage commitment, ask whether your payment will change if prime rate changes and how your amortization could be affected if rates rise.

My Advice

Variable-rate and adjustable-rate mortgages both move with prime rate, but they handle payment changes differently. A traditional variable-rate mortgage generally keeps the same payment while adjusting how much goes toward interest and principal. An adjustable-rate mortgage changes the payment whenever rates move in order to keep the mortgage on schedule.

Neither option is right for everyone. The key is understanding how each product works and choosing the one that best fits your budget, financial goals, and comfort level with changing payments. Contact me if you have more questions or if you want free personalized advice.