How much do you need for a down payment? You might have heard it’s 5%, or maybe you’ve heard it’s better to have 20%. Both are options in Canada, but they work quite differently.

In this article, I’ll walk you through how each option works, the pros and cons, and how to decide which one may fit your situation best.

What Is 5% Down?

A 5% down payment is the minimum required for many homes in Canada, especially for first-time buyers.

Here’s how it works. You put down at least 5% of the purchase price, and the remaining amount is covered by your mortgage. Because you are borrowing more than 80% of the home’s value, you are required to have mortgage default insurance (often through CMHC or other insurers).

Key points:

- Minimum entry point into the housing market

- Requires mortgage insurance

- Allows you to buy sooner with less savings

Many first-time buyers choose 5% down because it gets them into the market faster. Instead of waiting years to save a large down payment, they can start building equity sooner.

What Is 20% Down?

A 20% down payment means you are putting down one-fifth of the home’s value upfront.

With 20% or more down, your mortgage is considered “conventional,” which means you do not need mortgage default insurance.

Key points:

- No mortgage insurance required

- Lower loan-to-value ratio

- Often results in lower monthly payments

Why some buyers choose it:

Buyers who have more savings or who are selling a previous home often choose 20% down to reduce their borrowing costs and monthly payments.

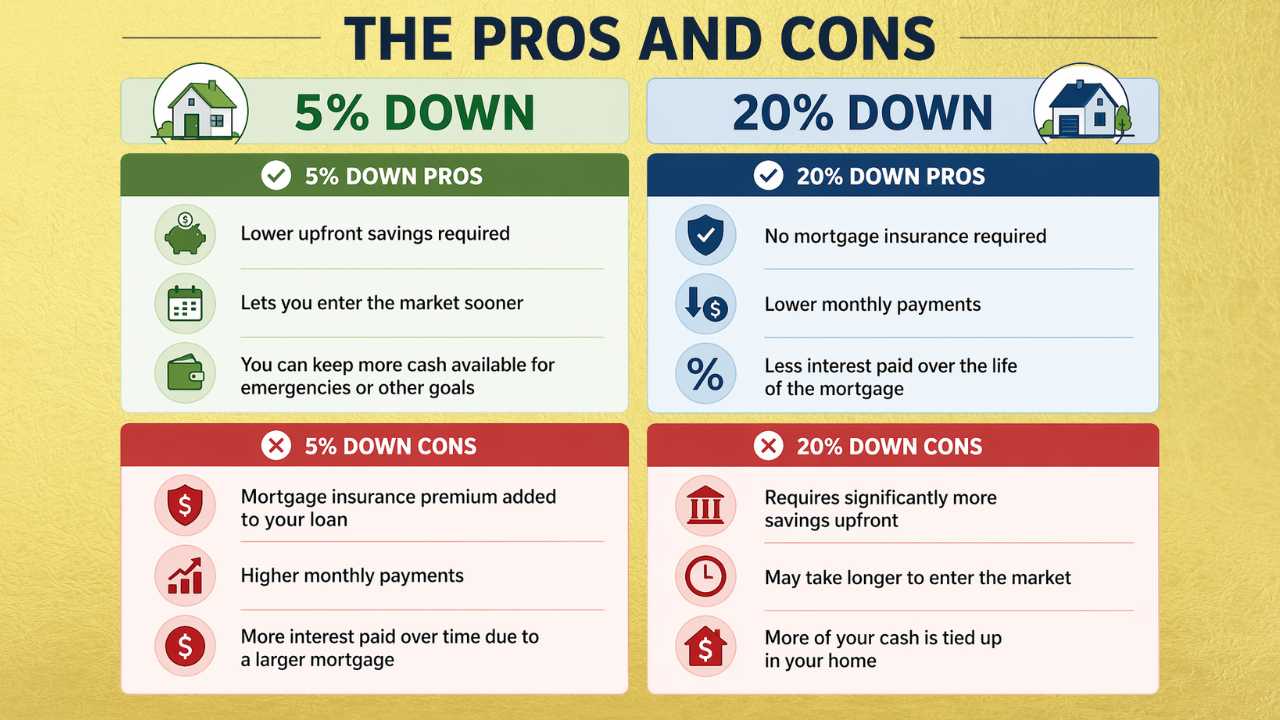

The Pros and Cons

5% Down Pros – This option means you require lower savings upfront, you can enter the market sooner, and you can keep the rest of your savings available for emergencies or other goals.

5% Down Cons – On the flip side, when you put down less than 20% you are required to have a mortgage insurance premium added to your loan, the monthly payments will be higher, and you will likely pay more interest over the life of your mortgage simply because it is bigger.

20% Down Pros – When you put 20% down you aren’t required to have mortgage insurance, you will have lower monthly payments, and you will likely pay less interest over the life of the mortgage.

20% Down Cons – However, this requires significantly more savings up front, which means you may take longer to enter the market, and you’ll have less left over for emergencies or other projects.

Which Option Is Better for First-Time Buyers?

This really depends on your situation and what you want to achieve.

If affordability and timing are your biggest concerns, 5% down can make a lot of sense. I work with many clients who want to stop renting and start building equity as soon as possible. In those cases, getting into the market earlier is often the priority.

If you have stable income but limited savings, 5% down can still be a strong option. It allows you to move forward without waiting years to build a larger down payment.

On the other hand, if you have the savings available and want lower monthly payments, 20% down may be the better fit. This is especially true for buyers who prefer more financial stability and less monthly pressure.

For some buyers, flexibility is key. Keeping extra savings on hand instead of putting everything into the down payment can provide peace of mind, especially in the first year of homeownership when unexpected costs can come up.

The Mistake Many First-Time Buyers Make

One mistake I see is buyers assuming that 20% down is always the “better” or “smarter” choice.

In reality, it depends on timing. If home prices are rising, waiting to save 20% could mean the home you want becomes more expensive while you wait.

I’ve seen buyers delay their purchase for years trying to reach 20%, only to find that prices moved faster than their savings. In some cases, they would have been better off buying earlier with 5% down.

How a Mortgage Broker Helps You Decide

When I sit down with clients, I look at your full picture: your income, your savings, your monthly comfort level, and your long-term goals.

We can compare what your payments would look like with 5% down versus 20% down. We can also talk about how much cash you should realistically keep aside after your purchase. The goal is to help you make a decision that feels comfortable and sustainable, not just one that looks good on paper.

If you’re trying to decide between 5% down and 20% down, the best next step is understanding what your mortgage options actually look like. Book a call with me to get started!