When you’re buying your first home, it can feel like every decision matters. And honestly, it does. One of the questions first-time buyers ask me is whether they should use a co-signer or a co-borrower to help qualify for a mortgage.

Both options can help you get approved. But they work very differently.

In this article, I’ll walk you through co-signer vs co-borrower in Alberta, explain how each option works, and help you figure out which one might fit your situation best.

What Is a Co-Signer?

A co-signer, often a parent or close family member, is someone who agrees to back your mortgage if you can’t qualify on your own.

They don’t live in the home and they’re not typically on title (ownership), so they don’t have any claim on the equity in the home. But they are fully responsible for the mortgage if you stop making payments.

Some buyers choose this option because they can’t qualify on their own due to low income or poor credit. Or they may simply want to buy now instead of waiting and have family support to do it.

I see this a lot with first-time buyers who are early in their careers or new to Canada.

What Is a Co-Borrower?

A co-borrower is someone who applies for the mortgage with you and shares both the loan and ownership of the property. This is very common with couples or siblings purchasing a home together. They are not just helping you qualify. They are buying the home with you. This is most often done by couples, but any two (or more) people can do it.

Having a co-borrower dramatically improves your buying power if you are both employed and have good credit.

You both apply together and use both of your incomes, debts, and assets to determine how much you qualify for. Both of your names go on the mortgage and on the title and you both have a claim on the equity in the home.

The Pros and Cons

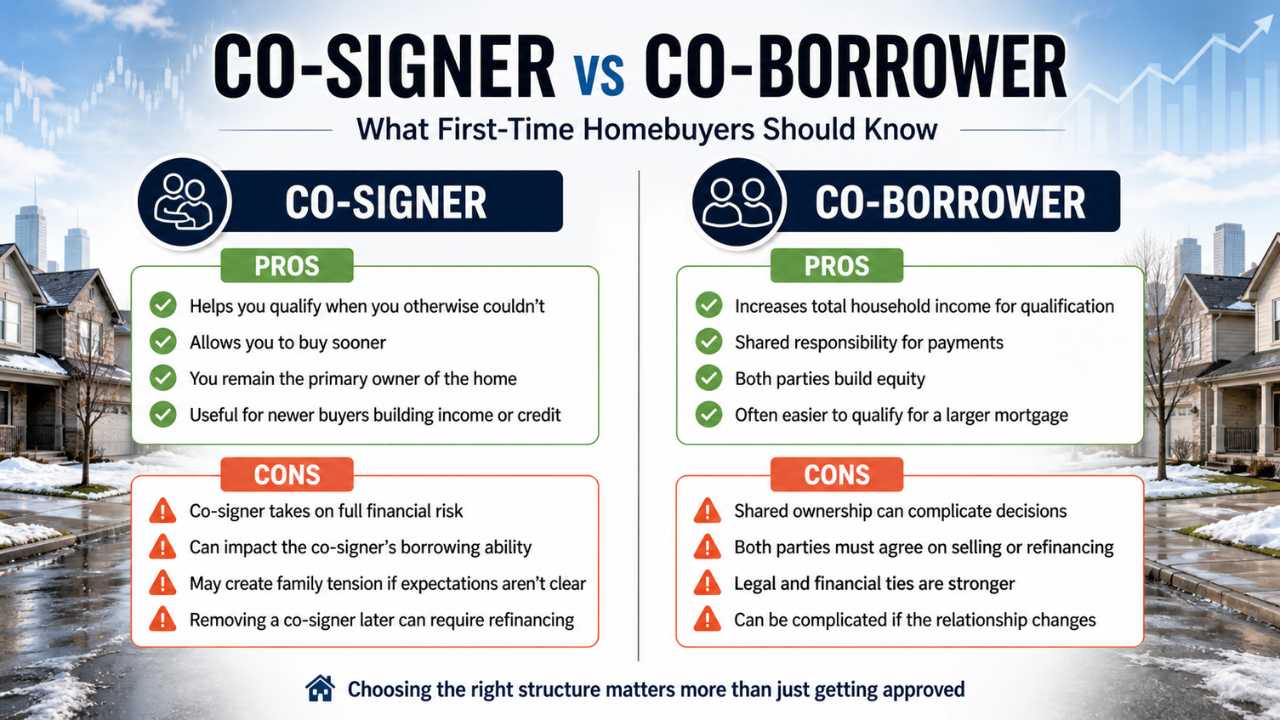

Co-Signer Pros

- Helps you qualify when you otherwise couldn’t

- Allows you to buy sooner

- You remain the primary owner of the home

- Useful for newer buyers building income or credit

Co-Signer Cons

- Co-signer takes on full financial risk

- Can impact the co-signer’s borrowing ability

- May create family tension if expectations aren’t clear

- Removing a co-signer later can require refinancing

Co-Borrower Pros

- Increases total household income for qualification

- Shared responsibility for payments

- Both parties build equity

- Often easier to qualify for a larger mortgage

Co-Borrower Cons

- Shared ownership can complicate decisions

- Both parties must agree on selling or refinancing

- Legal and financial ties are stronger

- Can be complicated if the relationship changes

Which Option Is Better for First-Time Buyers?

This really depends on your situation.

A co-signer may make more sense if:

- You want to own the home yourself

- You’re just short on income to qualify

- You have strong family support

- You expect your income to increase soon

For example, a young professional who just started their career may use a parent as a co-signer to get into the market earlier.

A co-borrower may make more sense if:

- You’re buying with a partner or spouse

- You plan to live in the home together

- You want to share costs and responsibilities

- You’re comfortable sharing ownership

For example, two buyers combining income to afford a better home or location.

If affordability is your main goal: both options can help, but co-borrowing often increases buying power more significantly

If flexibility is important: a co-signer arrangement may be easier to unwind later (though not always simple)

If long-term planning matters: think about what happens in 3–5 years, not just today

The Mistake Many First-Time Buyers Make

The biggest mistake I see? People focus only on getting approved. They don’t think about what happens after.

For example:

- Can the co-signer easily be removed later?

- What if the co-borrower wants to sell?

- How will this affect future borrowing for both parties?

Just because a lender says “yes” doesn’t mean it’s the best structure for your life. This is where a bit of planning upfront can save you a lot of stress later.

How a Mortgage Broker Helps You Decide

This is exactly where working with a mortgage broker can make a big difference.

When I help clients compare co-signer vs co-borrower options in Canada, I’m not just looking at approval.

I’m looking at:

- Your income and future earning potential

- Your long-term plans

- The risks for everyone involved

- How easy it will be to restructure later

Sometimes the best option isn’t the most obvious one. And often, there are alternative solutions people don’t even know exist.

My goal is to help you understand your options clearly so you can make a confident decision.

Next Steps

When it comes to co-signer vs co-borrower in Canada, both options can help you get into the market. But they are not the same. It comes down to your financial situation, your relationships, and your long-term plans.

- A co-signer supports your application without owning the home.

- A co-borrower shares both the mortgage and ownership.

If you’re trying to decide between co-signer and co-borrower, the best next step is understanding what your mortgage options actually look like. Send me a message and I’ll give you a call.